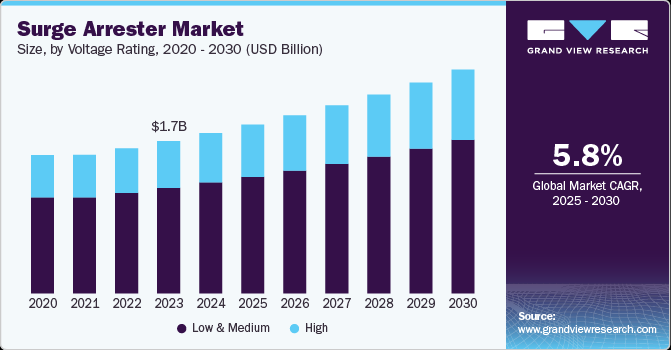

The global surge arrester market was valued at USD 1,844.46 million in 2024 and is expected to reach USD 2,573.50 million by 2030, growing at a CAGR of 5.79% from 2025 to 2030. This growth is driven by the increasing global demand for electricity and the complexity of modern power grids, which is leading to a higher adoption of surge arresters. Utilities and industrial facilities are increasingly investing in power quality solutions, further supporting market expansion. Additionally, governmental and regulatory initiatives aimed at modernizing grids, integrating renewable energy sources, and improving energy efficiency are also fueling the demand for surge arresters.

Key Market Trends & Insights

- Asia Pacific led the global surge arrester market with the largest revenue share of 40.0% in 2024. The region’s rapid industrialization, growing power transmission and distribution networks, and investments in renewable energy projects are driving market growth. In particular, the surging electricity demand in emerging economies such as India and China is prompting utilities to focus on improving power factor correction and grid stability, further boosting the demand for surge arresters.

- Low and medium voltage surge arresters are seeing significant demand across industrial, commercial, and utility sectors due to the growing need for energy efficiency, grid stability, and power factor correction. Factors such as rising electricity consumption, aging grid infrastructure, and government incentives promoting smart grids and energy conservation are contributing to this demand. Additionally, the integration of renewable energy, which requires power quality management, and the rise of industrial automation are accelerating the adoption of surge arresters.

- Industrial and Commercial Applications are key drivers for surge arrester demand, as industries rely on sensitive electrical equipment that must be protected from voltage surges and transient overvoltages. The rise of automation, robotics, and high-power machinery in industries such as oil & gas, mining, steel, and chemical processing underscores the need for reliable surge protection. Moreover, the growing trend of Industry 4.0 and the expansion of smart factories—where IoT-enabled systems and advanced control mechanisms are used—further intensifies the need for surge arresters to protect critical infrastructure and ensure operational continuity.

Order a free sample PDF of the Surge Arrester Market Intelligence Study, published by Grand View Research.

Market Size & Forecast

- 2024 Market Size: USD 1,844.46 Million

- 2030 Projected Market Size: USD 2,573.50 Million

- CAGR (2025-2030): 5.79%

- Asia Pacific: Largest market in 2024

Key Companies & Market Share Insights

Leading players in the surge arrester market include Siemens AG, ABB, GE, Schneider Electric SE, Eaton Corporation, and Hubbell Incorporated. These companies are investing in research and development to enhance the lifespan, reliability, and smart monitoring capabilities of surge arresters, incorporating technologies such as IoT and AI-driven predictive maintenance. Additionally, competition is being influenced by economies of scale, with major manufacturers expanding their production capacities to meet global demand while maintaining cost efficiency.

- In March 2024, Solar Power Systems, a leading clean energy solutions provider in the U.S., launched an extensive database of solar installers. This initiative aims to assist users in finding the most suitable solar company based on their location, offering reviews and insights to aid in the decision-making process for solar energy needs.

Key Players

- Siemens AG

- ABB AG

- GE

- Schneider Electric SE

- Eaton Corporation

- Hubbell Incorporated

- Megger Group Limited

- Furse Surge Protection

- Ingeteam

- CIRCUTOR

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

The surge arrester market is expected to experience steady growth due to increasing electricity demand, the expansion of grid infrastructure, and government initiatives to modernize grids and promote renewable energy. The Asia Pacific region will continue to dominate the market, while low and medium voltage surge arresters will remain key drivers in industrial, commercial, and utility sectors. The growing adoption of automation and smart grid technologies in industries like oil & gas, mining, and manufacturing will further increase the demand for surge protection solutions. Key players are focusing on innovation to enhance product reliability and integrate smart monitoring capabilities, ensuring they stay competitive in an evolving market.

No comments:

Post a Comment