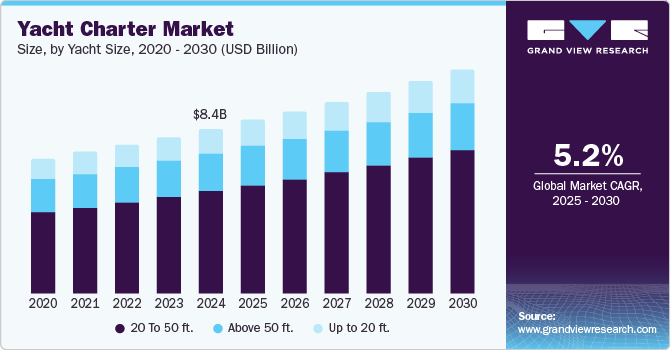

The global yacht charter market was valued at USD 8.35 billion in 2024 and is projected to reach USD 11.34 billion by 2030, growing at a CAGR of 5.2% from 2025 to 2030. This growth is primarily driven by rising disposable incomes and a growing interest in luxury marine tourism, as more individuals seek distinctive and high-end travel experiences.

The increasing popularity of recreational boating activities and the demand for customized services are key contributors to market expansion. Additionally, technological advancements in yacht design, navigation systems, and onboard amenities, combined with the development of yachting infrastructure, continue to support the industry’s upward trajectory.

Yacht charters allow individuals to rent yachts for leisure, offering opportunities to explore scenic destinations with luxurious onboard experiences. The market is increasingly shaped by digital platforms and mobile applications, which simplify the booking process. These solutions enable users to explore yacht options, compare prices, and make reservations in real-time, reducing the need for time-consuming offline coordination.

The shift toward personalized, exclusive leisure activities is further boosting demand among high-net-worth individuals. Many travelers are seeking private, immersive experiences, and yacht charters offer a unique way to visit secluded coastal areas. In parallel, eco-friendly innovations, such as sustainable propulsion systems, are gaining popularity, appealing to environmentally conscious customers.

Order a free sample PDF of the Yacht Charter Market Intelligence Study, published by Grand View Research.

Key Market Trends & Insights

- Europe led the global yacht charter market in 2024, accounting for the largest revenue share of 43.9%. The region benefits from a strong maritime tradition, established coastal tourism infrastructure, and popular destinations like the Mediterranean and Adriatic Seas. The rise in disposable income and consumer interest in marine tourism have made Europe a dominant force in the global charter industry.

- By yacht size, the 20 to 50-foot segment held the largest share at 62.3% in 2024. This segment offers a blend of affordability, efficiency, and comfort, making it ideal for families and small groups. Its shallow draft allows access to more anchorages, and its compatibility with wind sailing and renewable energy sources appeals to sustainability-minded travelers.

- By contract type, the bareboat charter segment is expected to grow at a CAGR of 4.2% during the forecast period. Bareboat charters offer flexibility and cost advantages, attracting experienced sailors who prefer to navigate independently. Advancements in navigation technologies have made it easier for users to manage charters without professional crews, increasing the appeal of this option.

- By yacht type, the motor yacht segment dominated with a revenue share of 87.3% in 2024. Their speed, fuel efficiency, and suitability for both leisure and competitive events make them a preferred choice. The ongoing rise in marine tourism and interest in recreational boating continue to support the strong demand for motor yachts.

Market Size & Forecast

- 2024 Market Size: USD 8.35 Billion

- 2030 Projected Market Size: USD 11.34 Billion

- CAGR (2025-2030): 5.2%

- Europe: Largest market in 2024

Key Companies & Market Share Insights

Major players in the yacht charter industry include Sunseeker International Ltd., The Moorings Limited, Camper & Nicholsons International Ltd., and others. These companies are focusing on innovation, personalized services, and expanding their fleets with modern and eco-friendly vessels.

- Sunseeker International Ltd. is known for its luxury performance motor yachts featuring advanced craftsmanship and design. Its product lineup includes the Manhattan, Predator, and Ocean series, tailored for high-end leisure experiences.

- Boat International Media Ltd. operates within the marine media sector, offering industry-specific publications and digital content related to luxury yachts, charter destinations, and lifestyle trends. It serves as a key information source for yacht owners, buyers, and enthusiasts.

Key Players

- Beneteau S.A

- Sunseeker International Ltd.

- The Moorings Limited

- Camper & Nicholsons International Ltd.

- Sunsail Worldwide Sailing Ltd.

- IYC

- Argo Nautical Limited

- Burgess Yacht

- Kiriacoulis Mediterranean Cruises Shipping S.A.

- Boat International Media Ltd.

- Yachtico Inc.

- Fraser Yachts Florida Inc.

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

The global yacht charter market is experiencing steady growth, driven by rising disposable incomes, the appeal of luxury travel, and advances in digital booking technologies. As travelers increasingly seek personalized, sustainable, and immersive experiences, the demand for yacht charters continues to climb. Europe remains the dominant regional market, while evolving preferences for eco-conscious vessels, smaller yachts, and bareboat charters reflect broader shifts toward flexibility and sustainability in leisure travel. With continuous innovations in yacht design and customer service, the market is well-positioned for long-term growth.