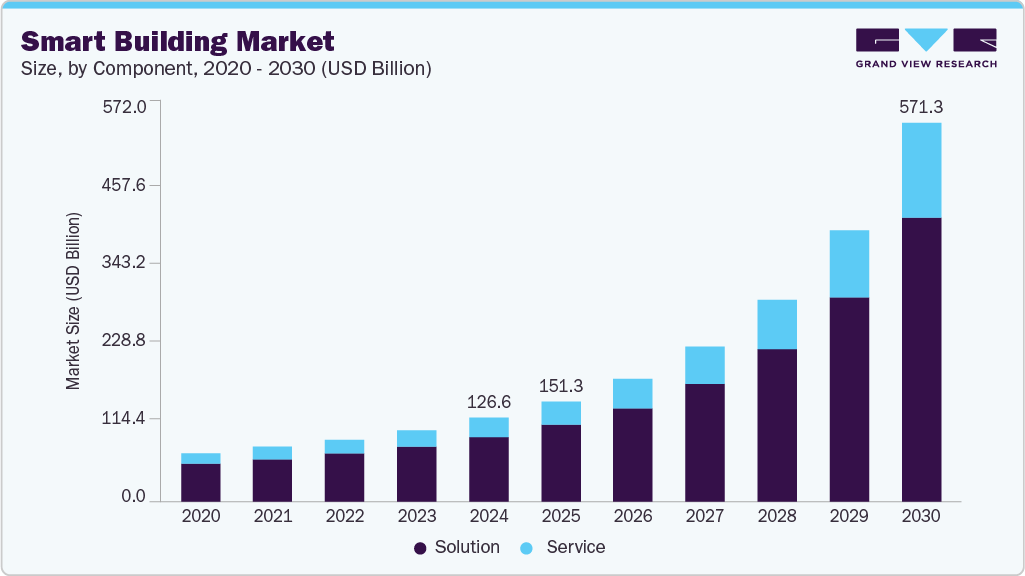

The global smart building market was valued at USD 126.58 billion in 2024 and is expected to reach USD 571.28 billion by 2030, expanding at a CAGR of 30.4% from 2025 to 2030. Growth in this market is primarily driven by rising adoption of IoT-enabled building management systems, an increasing focus on energy efficiency, and growing awareness surrounding sustainability initiatives.

Technological advancements in automation, data analytics, and AI-based energy management solutions are enabling real-time monitoring, predictive maintenance, and optimized climate control, which further fuel market expansion. The integration of IoT, AI, and advanced automation technologies to improve energy conservation, occupant comfort, and building performance continues to be a major catalyst for adoption.

Smart buildings combine interconnected systems—including lighting, HVAC, security, and facility management—within centralized platforms that support data-driven decision-making. Increasing urbanization, sustainability regulations, and mandates for energy-efficient buildings are prompting both government and private sector investments globally. Additionally, green building certifications and supportive policy frameworks are accelerating the widespread adoption of smart building technologies.

Technology innovations such as AI-powered analytics, edge computing, and digital twins are reshaping the industry. Building management systems (BMS) are evolving from passive monitoring tools to predictive, adaptive platforms capable of reducing operational costs and enhancing energy efficiency. Integration with smart grids and renewable energy systems also contributes to sustainability goals aligned with global carbon reduction strategies. Meanwhile, the shift toward hybrid work environments is increasing the demand for occupancy sensors and intelligent space management solutions.

Order a free sample PDF of the Smart Building Market Intelligence Study, published by Grand View Research.

Key Market Trends & Insights

- North America led the market with a 34.0% share in 2024, driven by expanding public and private investments and the rapid adoption of digital and automated building systems. IoT integration and advancements in digital infrastructure continue to enhance building automation and energy efficiency throughout the region.

- By component, the solution segment held more than 76.0% of revenue in 2024, supported by technologies such as AI-driven access control, biometrics, video surveillance, emergency communication, and cybersecurity. Growing emphasis on building safety, predictive maintenance, and mobile-based access is strengthening demand for integrated smart building solutions.

- By solution type, energy management is projected to record the fastest CAGR from 2025 to 2030, driven by technologies such as AI-enhanced HVAC systems, smart meters, demand-response programs, and lighting automation. Increasing net-zero targets, strict energy regulations, and predictive analytics adoption all contribute to segment growth.

- By service, the implementation segment dominated in 2024. Deployment of sensors, actuators, and microchips allows for extensive data collection to optimize operations. Integration of systems—such as fire alarms, HVAC, lighting, and power meters—into automation platforms supports improved reliability, occupant comfort, and reduced operating costs.

- By end use, the commercial sector led the market in 2024. Offices, retail centers, and hospitality venues are increasingly adopting smart systems to enhance sustainability, lower energy usage, and improve occupant experience. Regulatory pressure and rising operational costs are encouraging building owners to adopt advanced technologies.

Market Size & Forecast

- 2024 Market Size: USD 126.58 Billion

- 2030 Projected Market Size: USD 571.28 Billion

- CAGR (2025-2030): 30.4%

- North America: Largest Market in 2024

- Asia Pacific: Fastest growing market

Key Companies & Market Share Insights

Leading companies operating in the smart building industry include ABB Ltd. and Johnson Controls, along with emerging players such as Cisco Systems, Inc. and Emerson Electric Co.

- ABB Ltd. operates across four business segments—motion, robotics & discrete automation, electrification, and process automation—and serves 24 industries. Through ABB Technology Ventures (ATV), it has invested in multiple technology firms such as AFC Energy, Element Analytics, Numocity, and Stellapps. Its global service and dealer presence spans over 100 countries.

- Johnson Controls develops automation and control systems, including HVAC equipment, security systems, fire detection, refrigeration, and building automation solutions. The company serves sectors such as data centers, education, healthcare, transportation, government, and residential markets.

- Cisco Systems, Inc. specializes in hardware and software solutions across industries including smart buildings, utilities, healthcare, transportation, and financial services. Its offerings include cloud solutions, IoT technologies, AI systems, network infrastructure, and advanced security tools.

- Emerson Electric Co. provides automation and commercial/residential solutions, including valves, actuators, pneumatics, measurement equipment, HVAC systems, lighting, and control technologies.

Key Players

- ABB Ltd.

- BOSCH

- Cisco Systems Inc.

- Emerson Electric Co.

- Hitachi, Ltd.

- Honeywell International Inc.

- INTEL Corporation

- Johnson Controls

- KMC Controls

- LG Electronics Inc.

- Legrand

- Schneider Electric Corporation

- Siemens AG

- Sierra Wireless (Semtech)

- Telit

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

The global smart building market is on a strong growth trajectory, driven by the rapid adoption of IoT, AI, and automation technologies that enhance building performance, reduce energy consumption, and improve occupant comfort. As sustainability regulations intensify and organizations pursue net-zero goals, demand for intelligent energy management and integrated building systems will continue to rise. North America remains the leading market due to its advanced digital infrastructure, while Asia Pacific is emerging as the fastest-growing region. With technology evolving toward predictive and adaptive building management, smart buildings are poised to become a central component of future urban infrastructure worldwide.

No comments:

Post a Comment