The global home furnishing market was valued at USD 1,018.2 billion in 2024 and is expected to reach USD 1,703.86 billion by 2030, growing at a CAGR of 9.2% from 2025 to 2030. The demand for home furnishings is strongly influenced by the performance of the real estate sector, which drives the need for both new and replacement decor.

A robust housing market leads to increased home purchases and renovations, directly contributing to higher sales of furnishing and decor products. Moreover, rising disposable incomes, particularly in emerging economies such as China and India, are enabling consumers to invest more in home aesthetics. As environmental awareness grows, consumer preferences are shifting toward eco-friendly and sustainable decor items. This trend is prompting manufacturers to innovate using recyclable and natural materials.

Another trend shaping the market is the popularity of DIY home improvement and personalized home decor, with consumers increasingly opting for unique and customizable items that reflect individual styles. With urban living spaces becoming more compact, there is a growing preference for multifunctional furniture that combines style with practical space-saving features. Products such as modular sofas, folding tables, and convertible storage units are gaining traction.

Technological innovation is also becoming more prominent in the home furnishing industry. Consumers are showing interest in smart furniture, automated lighting systems, and other tech-integrated decor solutions that offer convenience and enhanced functionality. Additionally, limited indoor space has led to increased investment in outdoor decor, with many urban dwellers transforming their balconies, terraces, and patios into stylish and functional extensions of their homes.

Order a free sample PDF of the Home Furnishing Market Intelligence Study, published by Grand View Research.

Key Market Trends & Insights

- North America held the largest share of the global home furnishing market in 2024, accounting for 36.67% of total revenue. Consumers in the region are increasingly focused on improving their home environments, recognizing the link between living space and overall well-being. A strong housing market, including new construction and home sales, continues to fuel demand for furniture and decor.

- Home furniture dominated the product segment in 2024, contributing 50.76% of revenue. The growing pace of urbanization is a significant factor here. As per the United Nations, the global urban population is expected to reach 68% by 2050, up from 55% today. This shift is increasing the demand for residential furniture as urban housing developments continue to rise.

- In terms of distribution, online channels accounted for 34.94% of the home furnishing market revenue in 2024. The growing popularity of e-commerce is supported by features like virtual room previews, customer reviews, fast delivery, and easy returns, all of which enhance the online shopping experience and drive digital sales growth.

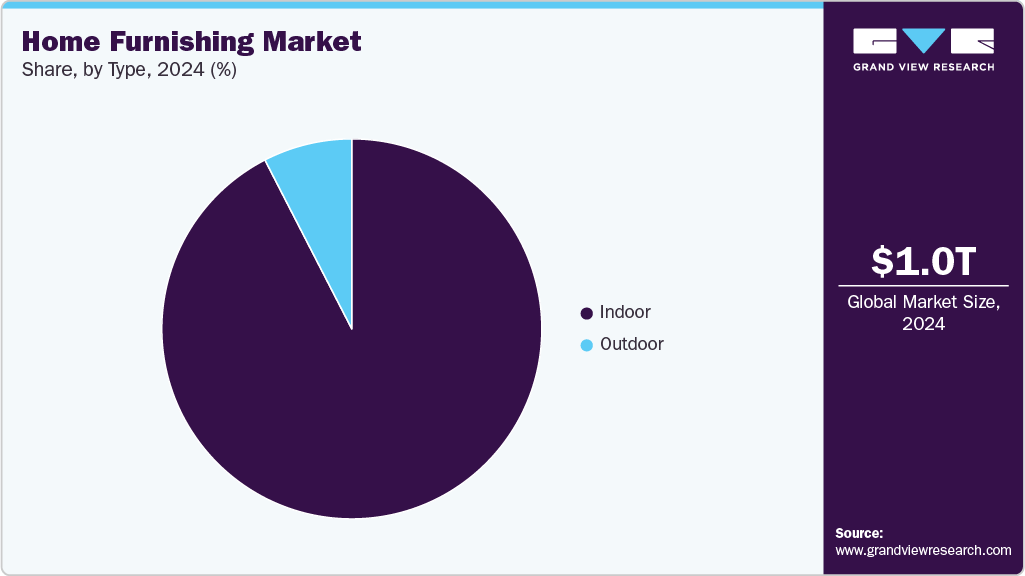

- Indoor home furnishings remained the dominant type in 2024, representing 92.44% of total market revenue. A growing trend is the integration of natural elements into indoor spaces, with the use of materials such as wood, stone, and indoor plants. Consumers are designing homes that accommodate multi-functional uses, blending work, relaxation, and social activities into shared spaces using modular and adaptive furniture.

Market Size & Forecast

- 2024 Market Size: USD 1,018.2 Billion

- 2030 Projected Market Size: USD 1,703.86 Billion

- CAGR (2025-2030): 9.2%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Key Companies & Market Share Insights

Companies active in the home furnishing space are adopting various strategies to increase market penetration and strengthen brand visibility. These include strategic partnerships, geographic expansions, and the introduction of new product lines. Key players are focusing on both physical store networks and digital platforms to reach a broader customer base, especially in emerging markets.

Key Players

- Wayfair Inc.

- IKEA

- Ashley Furniture Industries Inc.

- RH (Restoration Hardware)

- Williams-Sonoma, Inc.

- La-Z-Boy Inc.

- Raymour & Flanigan

- American Signature

- Oppein Home Group Inc.

- Jason Furniture (Hangzhou) Co., Ltd

- Steelcase Inc.

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

The global home furnishing market is set to witness robust growth through 2030, fueled by rising disposable incomes, urbanization, technological integration, and shifting consumer preferences toward sustainable and personalized living spaces. With growing interest in compact, smart, and eco-friendly solutions, manufacturers are innovating rapidly to meet evolving demands. The surge in e-commerce and the expansion of rental housing further contribute to the market’s momentum. As consumers continue to prioritize comfort, style, and functionality in their living environments, the demand for diverse and adaptable home furnishings is expected to remain strong worldwide.