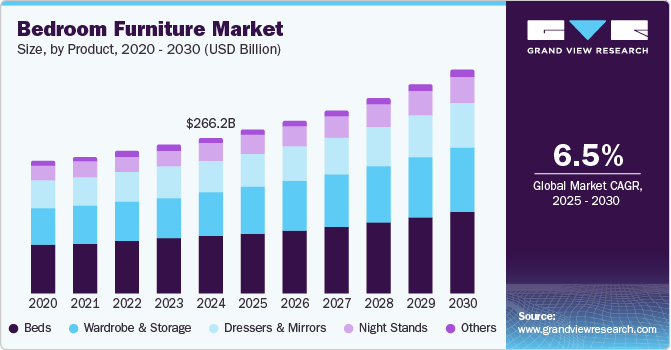

The global bedroom furniture market was valued at USD 266.15 billion in 2024 and is expected to reach USD 383.12 billion by 2030, growing at a CAGR of 6.5% from 2025 to 2030. This growth is primarily driven by increasing demand from urban consumers, rising disposable income levels in developing economies, and the convenience of purchasing a wide variety of bedroom furniture sets and individual items through online platforms.

Several key trends are shaping the market, including home redevelopments, the growing interest in home décor and accessories, furniture refurbishments, and the customization of bedroom furniture. The introduction of innovative, functional bedroom furniture designs with new styles has also contributed to the surge in demand. Designs incorporating biophilic elements, vintage themes, nostalgic patterns, and minimalist tech-integrated furniture are becoming increasingly popular. Additionally, many consumers are drawn to multifunctional furniture that meets changing lifestyle needs, further fueling market expansion.

There is also a rising demand for luxurious yet simple designs. These designs feature neutral color palettes and incorporate premium materials with ambient lighting, making them especially attractive to urban consumers. The growing trend toward multifunctional bedroom furniture, which adapts to the evolving needs of modern lifestyles, is also boosting market growth.

Additionally, there is growing interest in a wide range of bedroom furniture styles, including zen, japandi, retro, eclectic, Scandinavian, Bohemian, and many others. The market has also seen an increase in the availability of technology-driven tools, such as immersive virtual design experiences, which allow customers to digitally redesign their rooms and visualize the suitability of products. For instance, in February 2024, IKEA Australia introduced IKEA Kreativ, an AI-driven, mixed-reality experience that enables customers to reimagine and design their living spaces.

Order a free sample PDF of the Bedroom Furniture Market Intelligence Study, published by Grand View Research.

Key Market Trends & Insights

- Regional Insights: The Asia Pacific region held the largest revenue share of 39.5% in 2024. This market dominance is driven by growing demand from highly populated countries like India and China, rising disposable income, and the rapid expansion of the construction industry. Urban consumers in countries such as China, Japan, India, and Australia are significantly contributing to market growth. The region benefits from a diverse offering of modern designs, technology-driven products, and antique collections.

- Product Insights: The beds segment was the largest contributor to the global bedroom furniture market in 2024, accounting for 36.8% of total revenue. Growth in this segment is largely due to the introduction of innovative and design-forward products, as well as the rise in home redevelopments and the growing accessibility of these products through online stores. The increasing popularity of smart beds, which feature advanced technologies such as adjustable cushions, lighting, shape-shifting capabilities, and data collection features, has also contributed significantly to the market’s growth.

- Distribution Channel Insights: The offline distribution segment was the largest revenue share holder in the global bedroom furniture market in 2024. Consumers continue to favor offline shopping due to the convenience of examining products firsthand, assessing materials and quality, and engaging with store staff for advice. This preference has driven the growth of offline retail channels, especially as brands emphasize customer engagement through physical stores.

Market Size & Forecast

- 2024 Market Size: USD 266.15 Billion

- 2030 Projected Market Size: USD 383.12 billion

- CAGR (2025-2030): 6.5%

- Asia Pacific: Largest market in 2024

Key Companies & Market Share Insights

Leading companies in the global bedroom furniture market include IKEA Systems B.V., Ashley Global Retail, LLC, American Signature Inc., and Williams-Sonoma, Inc. These brands are focusing on strategies such as product customization, offering immersive virtual design experiences, and providing post-purchase services to address the evolving demands of consumers.

- IKEA Systems B.V. offers a broad range of bedroom furniture products, including beds, storage solutions, home textiles, and smart home products. The company continues to expand its reach through both its physical stores and online platforms.

- Raymour & Flanigan Furniture and Mattresses provides a diverse selection of bedroom furniture items, such as bedroom sets, beds, nightstands, armoires, and custom furniture. The company also offers accessories like home décor, lighting, and vanity sets.

Key Players

- IKEA Systems B.V.

- Ashley Global Retail, LLC

- RH (Restoration Hardware)

- WILLIAMS-SONOMA, INC.

- La-Z-Boy Incorporated

- Raymour & Flanigan Furniture and Mattresses

- American Signature, Inc.

- Oppein Home Group Inc.

- Jason Furniture (HangZhou) Co., Ltd

- Steelcase

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

The global bedroom furniture market is poised for steady growth, driven by increasing demand for stylish, functional, and customizable furniture solutions. Key factors such as rising disposable incomes, urbanization, and the popularity of innovative, multifunctional furniture are expected to sustain this growth. Additionally, the use of technology-driven tools like virtual design platforms is shaping the way consumers shop for bedroom furniture. Asia Pacific will continue to dominate the market, while companies are increasingly embracing strategies such as product innovation, customization, and enhanced customer engagement to stay competitive. As consumers’ preferences evolve, the market for bedroom furniture will likely see continued expansion in the coming years.