The global data center chip market was valued at USD 21.21 billion in 2024 and is projected to reach USD 42.74 billion by 2030, expanding at a compound annual growth rate (CAGR) of 12.5% between 2025 and 2030. This growth is primarily driven by the increasing demand for high-performance computing (HPC) and data-intensive applications, which require advanced chip technologies to process vast amounts of data efficiently.

The rapid adoption of cloud computing, big data analytics, and artificial intelligence (AI) has significantly accelerated the need for high-capacity, energy-efficient data center chips. These chips must support modern workloads by offering improved scalability, computational performance, and lower energy consumption. Innovations in chip architecture—such as ARM-based processors and purpose-built AI chips—are gaining traction across the industry. ARM chips, in particular, are being adopted due to their superior energy efficiency, which is critical for large-scale data center operations aiming to minimize costs.

The rising demand for AI and machine learning (ML) workloads is also fueling the need for chips capable of parallel processing and high-throughput computation. Furthermore, the expansion of edge computing—where processing occurs closer to the data source—is increasing the demand for chips with low latency, high processing capability, and reduced power usage.

A notable example is the January 2025 announcement by ZEDEDA, a U.S.-based edge management firm, which opened a new headquarters in Abu Dhabi, UAE. Supported by investments from Alpha Wave Incubation and Prosperity7 (a subsidiary of Aramco), the move reflects growing regional demand for AI and edge computing solutions in the Middle East. In addition, the ongoing rollout of 5G networks globally is amplifying the need for robust data center infrastructure capable of delivering real-time processing and low-latency communication, further supporting market expansion.

Order a free sample PDF of the Data Center Chip Market Intelligence Study, published by Grand View Research.

Key Market Trends & Insights

- North America held a dominant market share of approximately 41.0% in 2024, fueled by its leadership in cloud computing, AI, and big data analytics. Tech giants such as Amazon, Microsoft, and Google continue to drive demand for advanced data center chips to support massive computational workloads.

- By chip type, the processors segment led the market in 2024, accounting for nearly 42.0% of the global revenue. Ongoing advancements in processor architecture from companies like Intel, AMD, and ARM have led to higher processing speeds and improved energy efficiency, aligning with the energy-saving goals of modern data centers.

- By data center type, the large data centers segment dominated in 2024. As hyperscale infrastructure becomes essential for cloud service providers such as AWS, Microsoft Azure, and Google Cloud, the need for high-performance, efficient chips continues to rise.

- By application, the artificial intelligence (AI) segment led the market in 2024. The widespread adoption of machine learning, deep learning, and generative AI has heightened the demand for GPUs, TPUs, and AI-accelerator chips capable of supporting parallel computing and rapid inference.

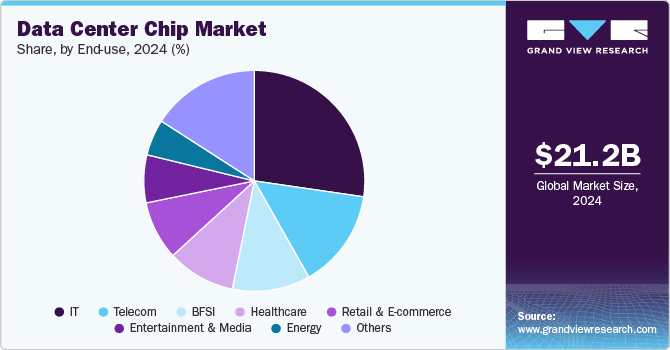

- By end-use, the IT segment dominated in 2024 due to the growing adoption of DevOps practices, CI/CD pipelines, and real-time responsive systems. These workloads require powerful chips that enhance virtualization, container orchestration, and system responsiveness.

Market Size & Forecast

- 2024 Market Size: USD 21.21 Billion

- 2030 Projected Market Size: USD 42.74 Billion

- CAGR (2025-2030): 12.5%

- North America: Largest market in 2024

- Asia Pacific: Fastest growing market

Key Companies & Market Share Insights

Prominent players in the global data center chip industry include NVIDIA Corporation, Micron Technology, Inc., STMicroelectronics, and Sensirion AG. These companies are investing in product innovation, strategic partnerships, and market expansion to strengthen their market positions.

Examples of recent initiatives include:

- Intel Corporation, in February 2025, launched the Intel Xeon 6 processors, delivering up to 2x performance improvements in AI workloads. These chips also feature Intel vRAN Boost, increasing capacity by 2.4x for radio access network (RAN) tasks.

- STMicroelectronics, also in February 2025, introduced a new chip developed in partnership with Amazon Web Services (AWS), utilizing photonics technology. These chips use light instead of electricity to increase processing speed while reducing power consumption in AI-driven data centers.

- In October 2024, NVIDIA unveiled the NVIDIA Grace CPU, a high-performance processor for data centers that emphasizes energy efficiency and scalability. The CPU is designed to meet the evolving computational demands of large-scale infrastructure.

Key Players

- Advanced Micro Devices, Inc.

- Alibaba

- Arm Holdings

- Broadcom Inc.

- Huawei Technologies Co., Ltd.

- IBM Corporation

- Intel Corporation

- Marvell

- Micron Technology, Inc.

- NVIDIA Corporation

- Qualcomm

- SAMSUNG

- STMicroelectronics

- Texas Instruments Incorporated

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

The global data center chip market is experiencing rapid growth, fueled by the increasing reliance on cloud services, AI, big data, and edge computing. As digital transformation accelerates across industries, demand for chips with enhanced computational capabilities, energy efficiency, and adaptability is rising. North America currently leads the market, while Asia Pacific is poised to grow the fastest. Key technological advancements—such as ARM-based processors, AI-specific chips, and photonics—are shaping the next generation of data center infrastructure. With continued innovation and strategic investments, the market is well-positioned to double in size by 2030, transforming how data is processed, stored, and analyzed globally.

No comments:

Post a Comment