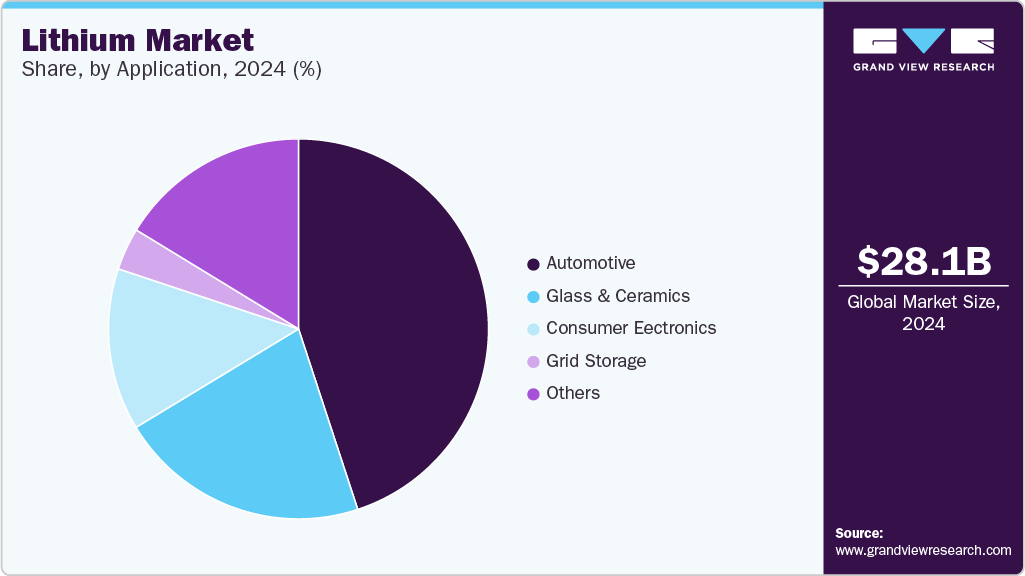

The global lithium market was valued at USD 28.08 billion in 2024 and is projected to reach USD 74.81 billion by 2030, growing at a CAGR of 18.2% from 2025 to 2030. This robust growth is primarily driven by the accelerating shift toward vehicle electrification, which is expected to generate substantial demand for lithium-ion batteries over the forecast period.

The automotive application segment is set to experience strong growth, fueled by increasingly stringent government regulations aimed at reducing carbon dioxide emissions from internal combustion engine (ICE) vehicles. In response, global automakers are investing heavily in electric vehicle (EV) production, which is directly increasing the demand for lithium and its derivatives.

In addition, government subsidies for EVs and growing investments in battery manufacturing are expected to further support lithium market expansion. The United States plays a significant role in global battery production—second only to China—making it one of the largest consumers of lithium globally.

As of 2024, the U.S. holds substantial lithium resources, estimated at between 14 million and 20–40 million metric tons, depending on evolving geological data. However, actual domestic lithium production remains limited. In 2024, the U.S. produced approximately 610 metric tons, accounting for just 0.3% of global output—far short of meeting its growing domestic demand, particularly from the EV sector.

Order a free sample PDF of the Lithium Market Intelligence Study, published by Grand View Research.

Key Market Trends & Insights

- Asia Pacific dominated the global lithium market in 2024, accounting for over 47% of total revenue. This leadership is driven by the region’s rapidly growing automotive, electronics, glass, and consumer goods industries—particularly in China, Japan, and South Korea. The region is expected to maintain its dominance and record the fastest CAGR in volume during the forecast period.

- By Application: The consumer electronics segment is anticipated to register the fastest revenue CAGR, exceeding 27.6% between 2025 and 2030. Rising global demand for electronic devices—such as smartphones, laptops, cameras, speakers, and portable radios—continues to drive lithium usage in this segment.

- By Product: The lithium carbonates segment is projected to grow at a notable CAGR in revenue terms from 2025 to 2030. Lithium carbonate (Li₂CO₃) is a key compound used in producing lithium hydroxide and pure lithium metal, and also plays a role in pharmaceutical applications, such as treating bipolar disorder.

Market Size & Forecast

- 2024 Market Size: USD 28.08 billion

- 2030 Projected Market Size: USD 74.81 billion

- CAGR (2025-2030): 18.2%

- Asia Pacific: Largest market in 2024

Key Companies & Market Share Insights

Several major players are shaping the global lithium market through production, innovation, and strategic expansion. Key companies include Albemarle, Ganfeng Lithium Co., Ltd., and Mineral Resources.

- Albemarle Corporation - Albemarle’s lithium segment develops lithium-based materials for a range of industries. The company manufactures lithium carbonate, hydroxide, chloride, and other specialized reagents such as butyllithium and lithium aluminum hydride. Albemarle also provides technical services, including support for handling reactive lithium products and recycling lithium-containing by-products.

- Ganfeng Lithium Co., Ltd. - Ganfeng serves various sectors, including EVs, energy storage, pharmaceuticals, chemicals, and 3C (Computer, Communication, and Consumer Electronics). The company has the capability to extract lithium from ore, brine, and recycled materials, offering more than 40 lithium and related metal compounds—making it one of the most diversified suppliers in the market.

Key Players

- Albemarle Corp.

- Ganfeng Lithium Co., Ltd.

- SQM S.A.

- Tianqi Lithium Corporation

- Livent Corp.

- Lithium Americas Corp.

- Pilbara Minerals

- Orocobre Limited

- Mineral Resources Group Co., Ltd.

Explore Horizon Databook – The world's most expansive market intelligence platform developed by Grand View Research.

Conclusion

The global lithium market is entering a high-growth phase, driven by the rapid expansion of electric vehicles, increasing adoption of consumer electronics, and rising demand for energy storage solutions. With a projected CAGR of 18.2% through 2030, the market is set to nearly triple in value. While Asia Pacific will continue to lead in both production and consumption, countries like the United States are actively working to enhance domestic lithium supply through government-backed investments and innovation. The ongoing integration of lithium into critical sectors—including automotive, electronics, and pharmaceuticals—will continue to drive market expansion, positioning lithium as a cornerstone of the global clean energy transition.